Compliance & Assurance

Compliance Monitoring that makes sense.

Map obligations to controls, risks and more to provide clarity and confidence.

Trusted by hundreds of clients globally

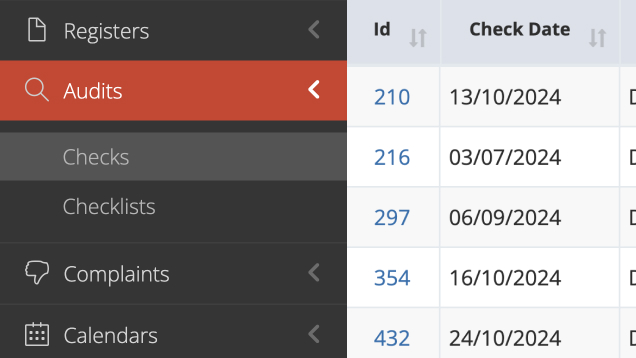

Stay audit-ready, always

Access a single source of truth at your fingertips, ensuring you're ready for every audit, all the time.

Streamline internal controls

Use pre-populated libraries to map risks to controls, assign ownership and track control testing.

Stop chasing, start analysing

Say goodbye to manual follow ups - automate reminders for tasks, findings, control tests and more.

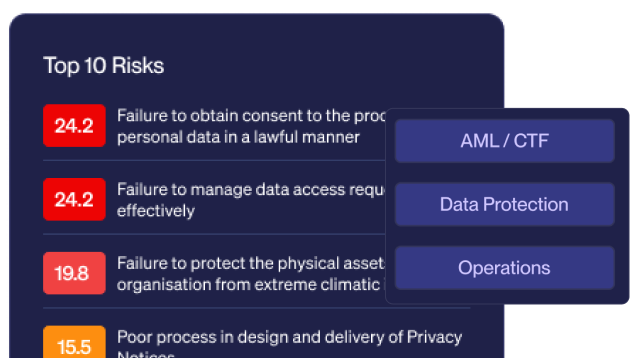

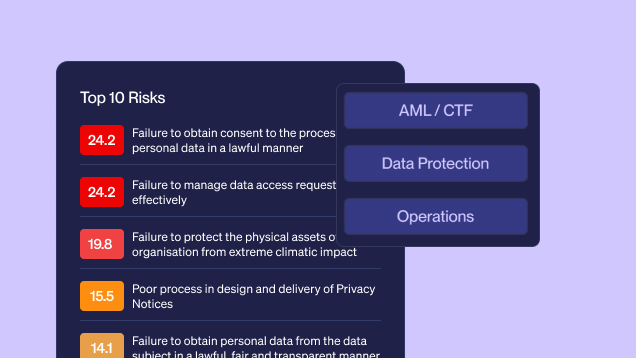

Report at the click of a button

Generate tailored reports on risks, controls and more with a single click.

Go live in days, not months

Launch quickly with pre-built templates and workflows that deliver immediate value from day one.

Roles

Related roles that benefit from our platform.

Keep compliance, legal, and finance teams aligned on regulatory obligations and control effectiveness.

Next Steps

One platform. Full visibility. Continuous compliance.

Schedule a 30-minute platform walk-through with our expert team.