Compliance Monitoring that makes sense.

Trusted by hundreds of clients globally

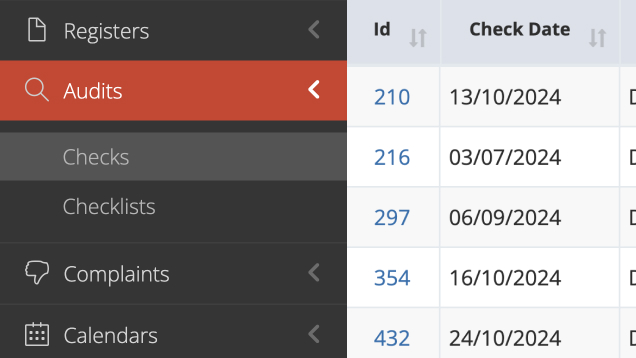

Stay audit-ready, always

Access a single source of truth at your fingertips, ensuring you're ready for every audit, all the time.

Streamline internal controls

Use pre-populated libraries to map risks to controls, assign ownership and track control testing.

Stop chasing, start analysing

Say goodbye to manual follow ups - automate reminders for tasks, findings, control tests and more.

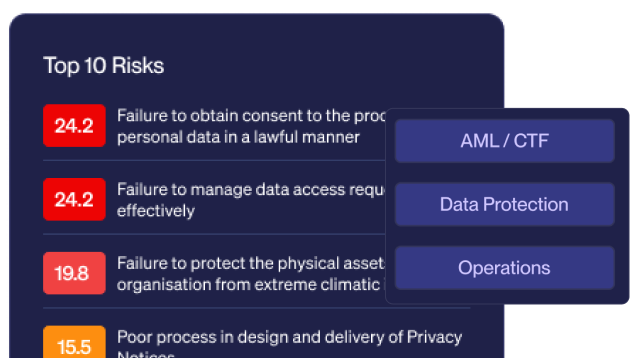

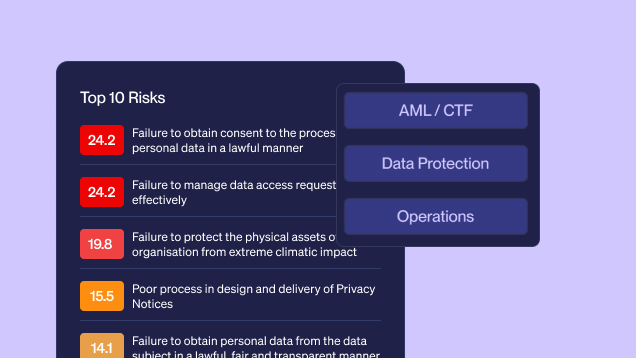

Report at the click of a button

Generate tailored reports on risks, controls and more with a single click.

Go live in days, not months

Launch quickly with pre-built templates and workflows that deliver immediate value from day one.

Customer Testimonials

First Choice Credit Union have been using calQrisk for over 5 years. Everything you need is in one place and all the important information is avaiable at the touch of a button. calQrisk takes the manual work of spreadsheets out of risk management and makes day to day reporting easy.

The calQrisk software has become a critical element of the Housing Agency’s Risk Management Framework. It has become a vital tool used by all members of staff, to ensure the effective monitoring of risks against our strategic objectives and the regulatory compliance of our organisation.

We have successfully implemented the solution for our RCSA, Risk Event and Issue Tracking processes resulting in efficiencies in the gathering, analysis and reporting of our risk information.

calQrisk is essential for any organisation that needs a risk management / compliance solution that will evolve with their business and provide them with the essential ingredients that will allow them manage their risks on an on-going basis.

With the calQrisk solution, we have a system in place to collate information into a single database. We have a complete organisational overview to manage and monitor risks, with risk owners spread across the organisation. As well as providing constructive and fit-for-purpose reports to many key stakeholders in a short period of time.

calQrisk was the obvious choice for enhancing our governance processes. From the outset, the solution has delivered immediate time savings and has significantly improved the efficiency and transparency of our operations. The onboarding process was smooth making the transition seamless.